Podcast: Play in new window | Download

Press play to listen to this article

The AI wave is creating the biggest corporate innovation opportunity in a generation. Most CVC programs are too busy copying the VC playbook to seize it.

Every few years, corporate venture capital goes through the same cycle: capital floods in, programs launch with ambitious mandates, and most quietly disappear within a few years. It isn’t because they made bad investments, but because they never built a durable reason to exist, one that survives leadership turnover and internal shifts in priority. We are in that cycle again, only this time the stakes are different.

In 2025, the global venture market hit $512 billion in deal value, its second-highest year on record. AI accounted for more than half of that total. In the U.S., AI captured nearly two-thirds of all VC deal value, which is up from just 10% a decade ago. Moving away from the sidelines, corporations are right at the center of the boom, with CVC-backed deal activity surging past previous highs. On paper, that looks like maturity. However, in practice, it is the earliest sign of a deepening identity crisis.

The Trap Hidden in the Boom

The pressure on corporate venture teams right now is not subtle. AI rounds that once took months to close are now closing in just days, with multi-billion dollar financings becoming routine. In that environment, the instinct inside every CVC team is the same: move faster, act more like an independent VC, and optimize for the metrics the board recognizes. That instinct is understandable, but it is also strategically dangerous.

The programs that collapse fastest are almost always the ones that most aggressively tried to compete with financial VCs on their own terms. In benchmarking IRR and chasing hot rounds, they lost the one advantage that set them apart: offering founders something no independent fund could. That advantage is not capital, but access to customers, distribution, and internal capabilities that can accelerate a company’s path to scale.

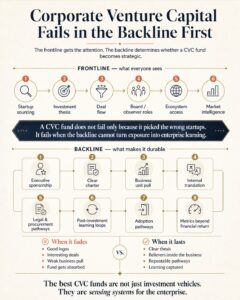

The question that needs to be asked is not whether CVCs need more discipline, but what they should be disciplined about. To answer, Harvard Business Review offers an explanation where the central finding directly challenges the dominant narrative: the best-performing CVCs do not succeed by eliminating the tension between startup speed and corporate processes. They succeed by designing mechanisms to make that tension “productive.”

The study describes what it calls a “frontstage/backstage” operating model: a fast, founder-oriented external face for deal-making and relationship-building, paired with a structured internal system for activating strategic value through business units. The programs that fail treat these as one job. The programs that last treat them as two distinct, carefully managed ones.

In our advisory work at Silicon Foundry, we see this pattern play out consistently: CVC programs that build lasting relationships with founders as well as lasting credibility with their own business units are the ones that invest in internal architecture as seriously as they do in external deal flow.

The Unfair Advantage Corporations Are Abandoning

No independent VC can offer a live enterprise customer, internal champions, and direct access to distribution, for the right startup, that can compress years of sales into months. The founders who choose a CVC over a financial VC are making a deliberate trade: a smaller check in exchange for strategic access.

But that trade only works when the access is enabling, not constraining. Meanwhile, the circular financing model, where corporations invest in AI companies that become major customers of the parent’s own infrastructure, is drawing both regulatory scrutiny and skepticism from founders. This model, which now defines Big Tech’s biggest AI bets, is raising questions about CVC capital coming with strings that look a lot like handcuffs.

The data reflects it. At Series D and beyond, CVC-backed companies carry median pre-money valuations of approximately $1.5 billion, roughly three times the median for non-CVC-backed counterparts. That premium is the market pricing of what strategic capital, when deployed correctly, actually delivers.

And the value runs in both directions. A peer-reviewed study published in Strategic Change found that CVC investments serve as a key mechanism for accelerating corporate AI adoption, enabling knowledge transfer that compounds over time in ways no internal R&D program alone can replicate. The corporations moving fastest on AI are winning not because they picked the best financial bets, but because they built early relationships with teams shaping the technology.

When CVC programs abandon that integration imperative in favor of pure financial benchmarking, the cost compounds quickly. Closure does not just end a fund, but poisons the internal conversation about corporate venturing for years afterward. The next leader who proposes a CVC program inherits the weight of “we tried that,” and the corporation loses its most important early-warning interface with the startup ecosystem precisely when it needs it most.

Consider the timing: McKinsey’s 2025 State of AI survey found that while 88% of organizations now use AI in at least one business function, only 39% report enterprise-level EBIT impact. The gap between experimentation and value creation is still wide, and well-structured CVC programs are one of the few mechanisms that can close it by linking emerging technologies to real business integration. Altogether, it is clear that the programs that collapse in this cycle will not just miss financial returns. They will miss the most important innovation window of the decade.

Three Questions Worth Asking Now

Going forward, corporate venture teams and their parent companies have to be honest with themselves and ask what they are actually building.

- Are we measuring the right thing?

Financial returns are the most legible CVC metric and the least useful proxy for whether a program is actually delivering for its parent. The programs that endure build measurement frameworks that track commercial introductions, knowledge transfer velocity, and strategic integration milestones. That conversation needs to happen before the first check is written, not after the first fund closes. - Have we separated the frontstage from the backstage?

The deal team that builds founder trust cannot also be the committee that routes every decision through multiple internal stakeholders. The HBR research is explicit: elite CVC programs build two operating models under one roof because they understand these are fundamentally different jobs requiring different norms, timelines, and accountability structures. - Is the program built to outlast the executive who championed it?

The single most common cause of CVC program death is not market failure or poor deal selection, but leadership turnover. A program built on the conviction of one executive, without structural embedding into the corporation’s broader innovation and strategy architecture, is not a CVC program. It is a side project with a term sheet.

The Identity Worth Having

The corporate venture programs that will matter in five years are not the ones that moved fastest or raised the largest funds. They are the ones that answered a more fundamental question clearly: “What can we offer a founder that no one else can?” The answer does not lie in speed or capital efficiency. It is the full weight of a corporation’s distribution, relationships, institutional knowledge, and strategic commitment, deployed in service of a startup’s growth, and translated back into the corporation as competitive intelligence, access to technology, and cultural proximity to where the future is being built.

Two out of three CEOs now say they plan to invest in corporate venture building in the year ahead. The infrastructure for the next cycle is being laid right now. The programs that define it will not be the ones that most faithfully copied the VC playbook. They will be the ones who had the confidence to build something no VC ever could.

That is the identity worth having. And it is the only one that lasts.

Elaine Barsoom is a Venture Partner at Silicon Foundry and a global leader in AI strategy and corporate innovation. She previously served as Global Head of Technology Innovation, Partnerships, and Strategy at Nike, and has spent over two decades helping Fortune 500 companies integrate emerging technologies into business strategy across industries.