Podcast: Play in new window | Download

Press play to listen to this article

Every major paradigm shift in consumer behavior has followed the same pattern: the infrastructure layer is built before adoption reaches scale. The foundations of the internet were laid decades before the web went mainstream, and the payment rails and logistics networks underpinning e-commerce were laid long before consumers were purchasing from direct-to-consumer brands.

We are now entering the infrastructure buildout phase for agentic payments. Card networks, AI model providers, and fintechs are actively investing in the protocols, rails, and interfaces that will allow AI agents to initiate, route, and settle financial transactions autonomously. With nearly half of consumers expressing interest in using agents for commerce and AI agent adoption projected to grow at a 45 percent CAGR over the next five years, the shift to agentic payments is inevitable. The commercial conditions are in place, but the question for financial institutions is what role they will play in the transition.

The dominant narrative suggests banks are at risk of being cut out, as stablecoin wallets and agent-to-agent payment systems begin to bypass the traditional financial infrastructure. While that outcome is possible, it underestimates what banks already own. Custody, execution, and the verified data layer are not legacy constraints. They are core capabilities that agentic payment systems will need to solve for. Building on existing bank infrastructure will be easier than rebuilding it. The agent economy will run on bank rails, as long as banks open access to them.

Agentic Payments as Governed Execution Systems

Agentic payments are systems in which AI agents execute financial transactions within pre-defined boundaries, and operate within regulatory requirements, payment network rules, and the constraints of existing payment infrastructure. Given the liability, auditability, and real-time risk controls that financial services demand, agentic payments will not operate outside compliance frameworks. They will operate within a rules-based workflow, with AI operating within the defined parameters. This architecture keeps banks at the center of the stack, not at the periphery.

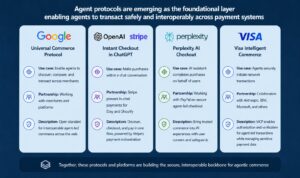

Mapping the Agentic Payments Stack

Agentic payments require three segments to function: card and payment networks, AI model providers, and banks. The first two are moving quickly. Visa has launched Intelligent Commerce with Anthropic, IBM, and Microsoft, allowing AI agents to transact as verified parties on its network. Mastercard has introduced Agent Pay and Agentic Tokens, enabling AI assistants to execute within predefined spending limits and merchant categories.

On the model provider side, Anthropic’s Model Context Protocol (MCP) is emerging as the interoperability standard for how agents connect to tools and data, and Google’s Agent-to-Payments Protocol (AP2), backed by more than 60 partners, is doing the equivalent work for payment authorization. OpenAI and Stripe have already demonstrated in-chat checkout that completes a purchase inside a conversational interface. Each of these players is building toward the same stack, and each assumes a bank sits underneath it. The question is which banks show up to occupy that position, and on what terms.

Three Structural Advantages Banks Still Control

The Custodial Layer of Trust

Every agentic payment system still relies on a trusted custodian of funds. While many players can build on top of the system, banks remain the only institutions that can provide that role within today’s regulatory frameworks.

As agents begin initiating payments, the need for a clear, accountable holder of funds is fundamental. That’s true whether those funds sit in a bank account or back a stablecoin. The custody layer does not need to be rebuilt. It needs access through permissioned, API-based access that allows agents to act within boundaries set by the customer, while banks continue to hold the underlying responsibility.

Control of Payment Execution

Banks control direct access to the settlement rails on which money moves: ACH, SWIFT, CHAPS, SEPA, and real-time rails, including FPS and RTP. Access to these rails is governed by banking licensure and settlement account relationships that cannot be disintermediated, regardless of how sophisticated the AI layer above becomes.

As agents assume greater responsibility at payment initiation, the bank’s role as issuer and execution counterparty becomes structurally more important. Agents operate at machine speed and volume, and they require credential validation, pre-authorization, and fund routing with greater precision and lower latency than human-initiated transactions demand today. A bank that builds agent-native execution interfaces becomes the default integration point for the stack above it.

The Decision Layer for Agents

Banks hold verified financial, transactional, and identity data that no other participant in the stack can match in depth or reliability. This includes transaction histories, account balances, behavioral patterns, counterparty relationships, and verified identity records that underpin trust across the system.

In an agentic model, this data becomes the input layer for every key decision: confirming available funds, assessing fraud risk, selecting the optimal payment credential, and maintaining audit trails. Banks that make this data accessible through secure, permissioned APIs can position themselves as the core data layer for the agent economy—those who don’t risk being bypassed by others building around them.

The Shape of What’s Next

The most likely path is co-evolution across banks, AI model providers, and card networking that build agentic payments infrastructure together, each contributing what they uniquely own. In that model, banks anchor the parts of the system that everything else depends on.

The idea that banks get cut out entirely is possible, but it would require rebuilding custody, execution, and trusted data outside today’s regulatory system. That’s a structural shift, not a product decision, and in practice, it’s far more efficient to build on what already exists.

The standards, protocols, and partnerships shaping this space are being defined in real time, and the institutions that engage early will help set the terms. Banks already hold the core pieces of custody, settlement infrastructure, and trusted data. The opportunity is to make them accessible in a way that fits how these systems will evolve.

Written by Christian Jaubert