Podcast: Play in new window | Download

Press play to listen to this article

Inside the portfolio tension between planting seeds and harvesting results

Corporate venture capital is no longer a tactical experiment. It’s a central lever for innovation and influence.

During the recent GCV Symposium panel in London, Silicon Foundry Managing Director Eli Promisel moderated a discussion with Managing Partner Terry Doyle of TELUS Global Ventures, Managing Partner Romy Schnelle of High-Tech Gründerfonds, and Managing Director Bernhard Mohr of Evonik Venture Capital, leading a conversation on whether CVCs should back high-risk, high-reward seedlings or drive late-stage investments for higher impact, financial returns, and strategic value.

CVCs are increasingly split between two investment approaches: early-stage bets that offer long-term strategic upside, and late-stage deals that promise faster impact with lower risk. Each path brings trade-offs in timelines, returns, and alignment with business needs. So the real question becomes: How can CVCs balance long-term strategic alignment with short-term value creation?

The Appeal of Growth-Stage Bets

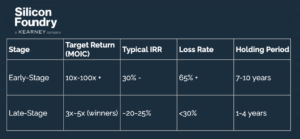

Historically, CVCs have opted for growth-stage investments to deliver near-term impact, achieve lower risks, and clearer ROIs. Unlike early-stage investments, late-stage investments offer an appealing strategic fit, featuring mature products, established teams, and clearer pathways to integration within existing business units. In the panel, Bernard Mohr stated that investing in seedlings compared to Series A/B investments may be seen as unappealing because seedlings can “take a long time to develop,” thus resulting in late gratification and greater exposure to various risks.

But these deals rarely shape the future. They may align with current priorities but often lack the capacity to define what’s next.

Why Early-Stage Still Matters

A recurring theme from the panel was the strategic importance of maintaining early-stage exposure, even as many CVCs double down on later-stage investments to deliver faster commercial outcomes. Despite the risk, early-stage investing remains critical to a strategically balanced CVC portfolio because these investments offer access, influence, and upside that growth-stage deals often can’t match.

For instance, Seed and Series A participation can deepen strategic optionality and strengthen long-term alignment with future growth areas the corporation may eventually need to own or integrate. Furthermore, backing young startups signals a commitment to innovation, attracting entrepreneurial talent, and positioning the corporation as forward-looking and ecosystem-driven, not just optimizing for today’s business.

The financial upsides are not to be ignored either. Despite high failure rates and limited liquidity through early 2025, many CVCs see early-stage bets as hedges against long-term irrelevance. After all, the power-law dynamics are compelling: a single outlier can define an entire portfolio. Take Coinbase, whose $0.20 Series A shares soared to $328.28 post-IPO. Since its last fundraising round in 2018, the company’s valuation has increased tenfold, and early investors from Union Square Ventures’ 2012 round have seen over a 4,000x return. On the other hand, Databricks delivered a 417x return within three years, coupled with a payback in less than six months . The upside, though rare, can be transformative. The question isn’t whether the risk is acceptable, but whether the CVC can afford not to play where the next wave is forming.

The Hybrid Model: Building a Barbell Portfolio

Ultimately, the most mature CVCs aren’t choosing one side; they’re building a barbell. This approach blends moonshot early-stage bets with growth-stage deals that deliver near-term wins.

During the GCV panel, leaders from TELUS Ventures, Evonik Venture Capital, and HTGF all described strategies that paired early investments in emerging tech with growth-stage bets aligned to current business lines. The idea: not to choose one side or another, but to use early-stage exposure to stay ahead of the curve, and growth-stage investments to drive tangible results today.

Implementing this model requires more than capital allocation. It demands:

- Tailored engagement models for different stages

- Separate metrics to track strategic and financial ROI

- Distinct internal stakeholders to support and advocate for each side of the portfolio

Several corporations have already successfully adopted this model. For example, Intel Capital historically has leaned towards later-stage investments without leading deals.

But that’s evolved.

Today, they pursue a dual strategy: they’re actively leading early-stage rounds, particularly in deep tech and forward-looking areas, while still investing in later-stage companies when there’s clear commercial traction or strategic fit. Thus, this hybrid approach enables Intel Capital to both cultivate emerging technologies at their earliest stages, while also accelerating the growth of more established companies that align with their strategic priorities.

Challenges in Execution

Balancing both early- and late-stage investing sounds compelling, but executing it is anything but simple. The real friction shows up in the day-to-day:

- Internal Pushback: Business units often prioritize immediate priorities, while CFOs expect predictable ROI, pressuring teams to favor safer, later-stage bets.

- Governance Complexity: Different stages require different cadences, diligence standards, and reporting structures, which can strain internal processes.

- Talent Mismatch: Sourcing and supporting early-stage startups demands a different skill set than managing growth-stage investments. Most CVC teams aren’t built to do both equally well.

Typically, high-performing teams struggle to consistently access top founders, decode early signals, and stay in sync with what elite VCs are seeing. However, this is where Silicon Foundry has become a trusted partner to leading CVCs, helping overcome the challenges of balancing early and late-stage investing. We’ve supported corporates in deploying and managing over $1 billion in venture funding and have a clear grasp of the operational friction that slows even the best CVC efforts.

For instance, we’ve talked to a top automotive CVC exploring sustainability and anticipated it would take up to two years to build internal conviction: researching trends, aligning leadership, developing a thesis, and understanding the competitive landscape.

But that’s where Silicon Foundry naturally provides a solution for speed and clarity.

Due to our unique position in the venture ecosystem, we work across dozens of sectors — from pharma and mobility to fintech and consumer — and bring immediate cross-market intelligence, test frameworks for investment theses, and curate exposure to the right founders and co-investors. Therefore, we would significantly compress the timeline and bring precise outcomes in a timely fashion.

As an embedded partner and natural extension of the CVC team, we help CVCs bridge the operational and strategic gaps that often slow progress:

- Thesis to Execution: Accelerate decisions with market validation and internal alignment.

- Governance Support: Navigate cadence, decision rights, and reporting by stage.

- Talent Extension: Expand team capacity with venture-native networks and execution muscle.

- Signal Amplification: Stay ahead of the curve with insight into what elite VCs are seeing and doing right now.

Rethinking Impact

The most resilient and future-ready CVCs won’t pick a side. They’ll build systems to extract value across the arc of innovation. Balancing seeds and harvests isn’t just a nice-to-have—it’s becoming table stakes.

Strategic foresight and operational discipline aren’t opposites. They’re complements. The question isn’t early vs. late. It’s whether your portfolio is designed to do both, and whether your team is built to deliver.